Financial Safeguards for Bipolar Overspending in Marriage

Quick answer: The safest financial safeguards for bipolar overspending in marriage are planned during stability, written clearly, consent-based whenever possible, and focused on protecting essentials first: housing, food, medication, utilities, transportation, debt payments, and crisis support. They are not punishment. They are a structure for the days when mania, hypomania, depression, impulsivity, or fear may make money decisions harder.

Important note: This article is for education and caregiver support only. It is not medical, legal, tax, credit, financial, relationship, or emergency advice. Bipolar disorder should be treated with professional care. If someone is suicidal, threatening harm, psychotic, violent, unsafe, or in immediate danger, call emergency services. In the United States, call or text 988 for crisis support.

Financial and legal note: If debt, joint accounts, credit damage, divorce, housing, domestic violence, coerced debt, identity theft, or financial abuse are involved, consider speaking with a qualified attorney, nonprofit credit counselor, financial advisor, domestic violence advocate, or other appropriate professional. Do not take control of another adult’s accounts, credit, devices, or property unless you have clear consent or legal authority.

At a Glance: What to Do Now vs. What to Build During Stability

| Situation | Urgent Step | Stability Step |

|---|---|---|

| Essential bills may be missed | Protect rent or mortgage, utilities, food, medication, and transportation first. | Create a separate bills account with automatic payments and limited access. |

| Active manic spending is happening | Pause arguments, protect shared essentials, and avoid making major decisions at 2 a.m. | Agree on spending thresholds, purchase delays, and a trusted check-in person. |

| New debt appears | Document balances, due dates, interest rates, and account names without blame. | Create a debt recovery plan with a nonprofit credit counselor or qualified professional. |

| Credit damage is possible | Protect your own credit report and ask creditors what options exist. | Discuss credit freezes, fraud alerts, lower limits, and account alerts during stability. |

| Money is being used to control or threaten | Prioritize safety and contact a domestic violence advocate if needed. | Build a safe exit or protection plan with professional support. |

| They refuse help | Do not try to become the doctor, banker, therapist, and crisis team alone. | Create a written support plan that includes treatment contacts and crisis steps. |

The key difference is this: crisis is for protecting essentials. Stability is for building agreements. Trying to create a complete financial system during an active episode often leads to more conflict, shame, and panic.

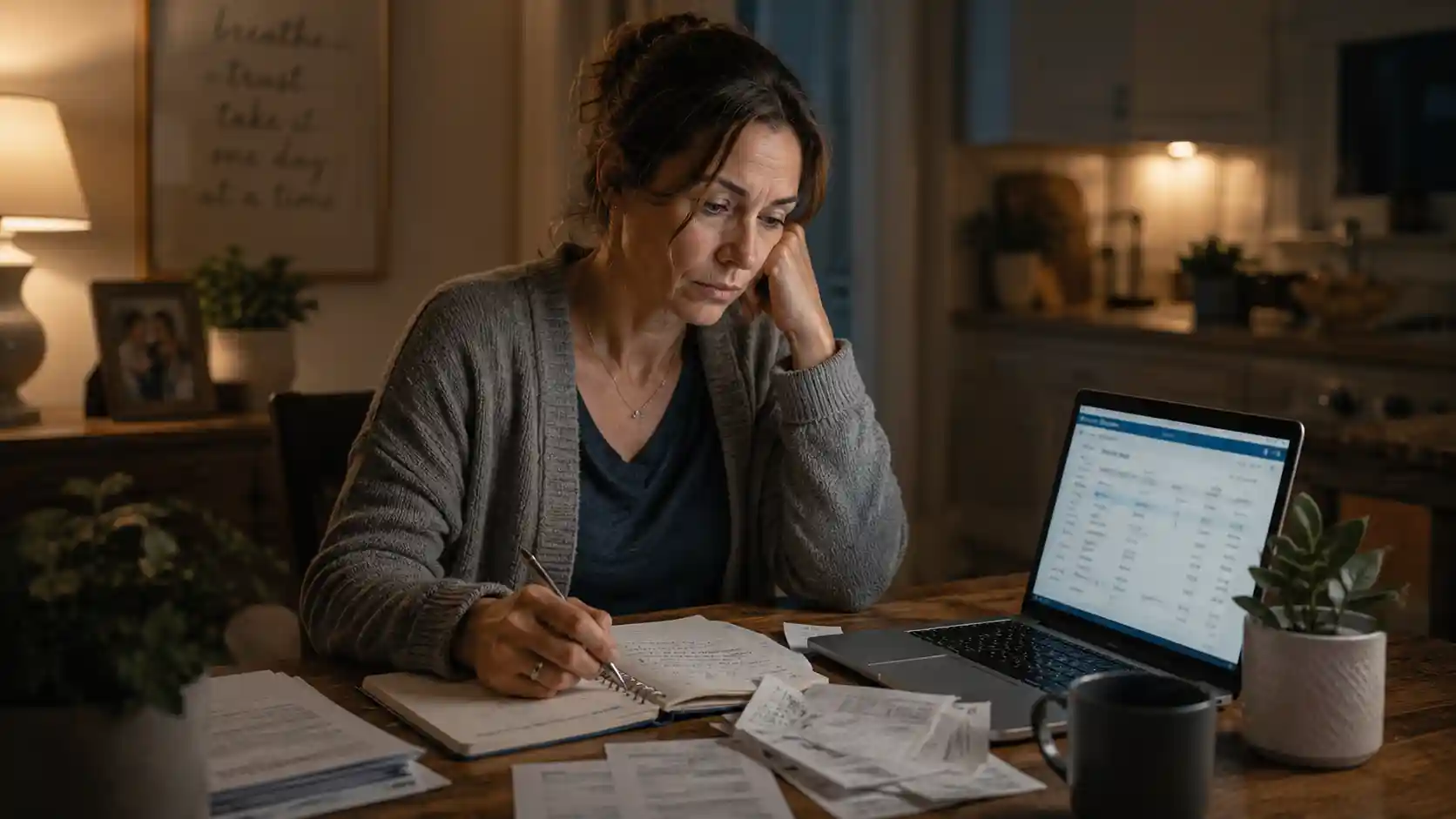

The Night I Realized Love Was Not a Financial Plan

For a long time, love felt like trusting harder.

The explanation sounded possible. The apology felt sincere. The spending seemed like something that might stop once the episode passed. Part of me believed that if I stayed calm enough, patient enough, and understanding enough, we could somehow out-love the damage.

Then I opened the banking app in the middle of the night.

There were charges I did not recognize. Subscriptions. Online orders. A hotel deposit. Three purchases from the same store. Small amounts, then bigger ones, then one amount that made my stomach drop.

I remember staring at the screen and whispering, “Please no,” as if the numbers might rearrange themselves if I asked nicely.

They did not.

That was the night I learned something I wish someone had told me earlier: when bipolar symptoms affect money, the damage is not only financial. It can affect safety, trust, sleep, resentment, shame, debt, housing, and the relationship’s ability to recover.

And still, I need to say this clearly: financial safeguards are not punishment. They are not parental control. Done well, they are consent-based protections created during stability, so both people know what to do when symptoms make financial decisions harder.

Can Bipolar Mania Cause Overspending?

Yes, some people with bipolar disorder experience impulsive or risky financial behavior during mania or hypomania. That can look like shopping sprees, gambling, risky investments, sudden business ideas, large gifts, travel, subscriptions, loans, or repeated purchases that feel urgent in the moment.

Not everyone with bipolar disorder overspends. Bipolar disorder does not automatically make someone irresponsible with money. But when overspending becomes part of a manic, hypomanic, depressive, mixed, or impulsive pattern, couples need more than promises and apologies. They need a plan.

The National Institute of Mental Health describes mania as involving changes in mood, energy, activity, sleep, thoughts, and behavior. These changes can affect judgment and daily functioning. That is why financial safeguards work best when they are created before the next crisis, not in the middle of one.

Financial Safeguards vs. Financial Control

This distinction matters. A lot.

A financial safeguard protects essentials, reduces damage, and respects dignity. Financial control removes independence, creates fear, hides information, or uses money to dominate someone.

| Financial Safeguard | Financial Control |

|---|---|

| Created during stability with clear discussion | Forced during crisis through fear, threats, or humiliation |

| Protects rent, food, medicine, utilities, and debt payments | Uses money to punish, shame, or isolate |

| Has written limits and review points | Has secret rules that keep changing |

| Allows personal spending money when possible | Removes all independence or access to basic needs |

| Involves professionals when legal or debt issues are serious | Avoids outside help so one person keeps all power |

| Protects both people’s safety | Makes one partner trapped, afraid, or dependent |

If you are unsure whether a safeguard has crossed into control, ask: “Does this protect essentials and dignity, or does it remove safety and independence?”

If there are threats, intimidation, coercion, isolation, withheld access to basic needs, or fear of leaving, this may be financial abuse rather than a bipolar caregiving issue. In that case, a domestic violence advocate or attorney may be more appropriate than a budgeting conversation.

Why Bipolar Overspending Can Hit a Marriage So Hard

Money in marriage is rarely just math. It can represent safety, trust, freedom, fairness, parenting, housing, retirement, and the future you thought you were building together.

When bipolar overspending or manic spending enters the relationship, the caregiver may feel pulled between compassion and panic. You may understand that symptoms are involved, but still feel devastated by the damage.

Common impacts include:

- missed rent, mortgage, utility, or car payments;

- credit card debt or personal loans;

- drained savings;

- secret accounts or hidden purchases;

- subscription pileups;

- gambling or risky investments;

- arguments about trust;

- fear of the next episode;

- caregiver burnout;

- shame for the partner who spent after symptoms settle.

The goal is not to make the person with bipolar disorder feel like a child. The goal is to protect the marriage from repeated financial emergencies that neither person can emotionally survive forever.

The First 24 Hours After a Manic Spending Episode

The first day after discovering manic spending is not the time to solve the whole marriage. It is the time to stabilize.

| Priority | What to Do | What to Avoid |

|---|---|---|

| Safety | Check for suicide risk, threats, violence, psychosis, or immediate danger. | Do not treat a crisis as a normal budgeting fight. |

| Essentials | Protect housing, food, medication, utilities, and transportation. | Do not spend the first hours arguing about every purchase. |

| Documentation | List charges, dates, accounts, due dates, and balances. | Do not delete records in anger. |

| Damage control | Contact banks, credit card issuers, merchants, or creditors to ask what options exist. | Do not make promises to creditors you cannot keep. |

| Support | Contact a clinician, trusted support person, credit counselor, attorney, or advocate when needed. | Do not try to carry the entire crisis alone. |

Use calm, factual language. “We need to protect rent and medication first” is more useful than “How could you do this again?”

If symptoms are still active, keep the conversation short. You can return to the deeper repair work when there is more stability.

Step 1: Protect Essential Bills First

The first financial safeguard is not a fancy budget. It is protecting the things that keep the household functioning.

Essential bills may include:

- rent or mortgage;

- utilities;

- food;

- medication and treatment costs;

- transportation;

- insurance;

- minimum debt payments;

- child-related expenses;

- phone or internet access needed for work, school, or care.

During a calm period, some couples create a separate bills account. Income for essential expenses goes there first. The account is used for survival bills, not impulse spending. Access rules should be discussed clearly and reviewed over time.

A simple structure may look like this:

| Account | Purpose | Access Idea |

|---|---|---|

| Bills account | Rent, utilities, insurance, food, medication, transportation | Protected access and automatic payments |

| Personal spending account A | Everyday personal spending for one spouse | Clear amount, no shame, no interrogation |

| Personal spending account B | Everyday personal spending for the other spouse | Clear amount, no shame, no interrogation |

| Emergency fund | Housing, safety, food, medication, crisis travel, legal or counseling help | Protected and not used for impulse purchases |

This is not about one person becoming the financial parent. It is about making sure one episode does not wipe out the household’s basic needs.

Step 2: Create a Written Spending Threshold

A spending threshold is an agreement about when a purchase needs a pause or a second conversation.

For example:

- Any non-essential purchase over a set amount waits 24 or 48 hours.

- No new credit cards, loans, payment plans, or subscriptions without a calm conversation.

- No major travel, business, investing, or vehicle decisions during suspected mania or hypomania.

- Online shopping carts must sit overnight before checkout.

- A trusted support person can be contacted when spending feels urgent or unusually exciting.

Use language like this:

“When we are both stable, we agree that any non-essential purchase over our threshold waits 48 hours. This is not about permission. It is about protecting our household from decisions we may regret later.”

The amount itself should fit your household. A couple with tight finances may need a small threshold. A couple with more savings may choose a higher threshold. The principle is the same: slow down money decisions when symptoms may be speeding everything else up.

Step 3: Add Friction Before Debt Happens

Friction is anything that makes impulsive spending less automatic. It does not remove all independence. It creates a pause between the urge and the purchase.

Examples include:

- removing saved cards from shopping apps;

- turning off one-click purchases;

- lowering credit limits where appropriate;

- using account alerts for large transactions;

- setting daily card limits if your bank allows it;

- keeping only one low-limit card for daily use;

- using cash or debit for discretionary spending;

- blocking gambling or shopping sites with consent;

- using automatic bill payments for essentials;

- keeping emergency funds separate from everyday spending.

Friction works best when it is agreed to during stability. It works poorly when introduced through panic, accusation, or secret control.

Step 4: Protect Your Own Credit

If you are worried about new accounts, identity theft, coerced debt, or credit damage, protect your own credit report. A credit freeze restricts access to your credit report, which can make it harder for new credit accounts to be opened in your name.

In the United States, the Federal Trade Commission explains that a credit freeze is free to place and lift, and that you must contact all three major credit bureaus: Equifax, Experian, and TransUnion. USAGov also explains that a freeze can be placed or lifted online, by phone, or by mail.

Important limits:

- A credit freeze protects your credit report. It does not stop spending on existing cards.

- You generally cannot freeze another adult’s credit without legal authority.

- A fraud alert may be useful if identity theft is suspected, but it is not the same as a spending boundary.

- If your name is on a joint account, speak with the bank or creditor about your options.

- If coerced debt or abuse is involved, speak with an attorney, domestic violence advocate, or qualified credit counselor.

Helpful official resources:

Step 5: Deal With Debt Without Shame or Denial

After bipolar overspending, debt can become emotionally loaded very quickly. One person may feel betrayed. The other may feel ashamed, defensive, terrified, or numb. Both people may avoid looking at the numbers because the truth feels too heavy.

But debt does not disappear because no one opens the statement.

Start with a simple debt inventory:

| Debt | Balance | Minimum Payment | Due Date | Interest Rate | Next Step |

|---|---|---|---|---|---|

| Credit card | Write current balance | Write minimum | Write date | Write APR if known | Call issuer or plan payment |

| Personal loan | Write current balance | Write payment | Write date | Write rate if known | Ask about hardship options if needed |

| Medical or treatment bill | Write current balance | Write payment | Write date | Write if applicable | Ask about payment plans |

| Buy now, pay later | Write total owed | Write next payment | Write date | Write fees if known | Stop new plans until stable |

| Overdraft or bank fees | Write total | Write required payment | Write date | Write fee details | Contact bank if needed |

If the debt is serious, do not rely only on advice from social media or random debt relief ads. Consider a nonprofit credit counselor, such as the National Foundation for Credit Counseling, or another reputable organization. If bankruptcy, foreclosure, divorce, tax debt, or lawsuits are involved, legal guidance may be necessary.

Step 6: Build a Stability Agreement Before the Next Episode

A stability agreement is a written plan created when the person with bipolar disorder is more stable and able to participate. It should be respectful, practical, and reviewed regularly.

It can include:

- early warning signs that spending risk is increasing;

- sleep changes that usually come before financial risk;

- who can be contacted if spending becomes unsafe;

- which bills must be protected first;

- what spending threshold triggers a pause;

- what accounts are used for essentials;

- which purchases wait 24 or 48 hours;

- what to do if debt appears;

- what to do if the caregiver feels unsafe;

- when to contact the treatment team or crisis support.

This type of agreement connects closely to a broader bipolar emergency plan. Money should be part of the crisis plan because financial damage can become a safety issue, a housing issue, and a relapse trigger.

Money Scripts for Hard Conversations

Money conversations after bipolar manic spending can easily become blame, defense, or panic. Scripts help you stay calm and specific.

When starting the plan during stability

- “I want us to talk about money while things are calm, not during the next emergency.”

- “This is not about punishing you. It is about protecting rent, medication, food, and our future.”

- “Can we write down what should happen if spending starts to feel urgent or out of character?”

- “I want the plan to protect your dignity and my sense of safety.”

- “I do not want to become the money police. I want us to build a system that reduces panic.”

When spending is active

- “I am not going to argue about every purchase right now. I am focused on protecting essentials.”

- “This feels urgent to you, but I am not comfortable making a major financial decision tonight.”

- “Let’s pause new purchases and revisit this when we have both slept.”

- “I care about you, and I am worried because this spending feels connected to symptoms.”

- “I am going to contact support because I cannot manage this alone.”

When they ask for money

- “I care about you, but I cannot give cash today.”

- “I can help with food, medication, or transportation, but I cannot cover this purchase.”

- “I know this feels stressful. My answer is still no.”

- “I am willing to help make a plan, but I am not willing to take on new debt.”

- “I cannot rescue this financially in a way that puts housing or bills at risk.”

After the episode

- “I want to talk about what happened without shaming you.”

- “We need to look at the numbers because avoiding them will make the damage worse.”

- “I am hurt and scared, and I still want us to repair this with support.”

- “Let’s separate blame from responsibility. Symptoms may explain part of this, but we still need a recovery plan.”

- “I need more than an apology. I need a safeguard before I can feel safe again.”

What Not to Say About Money After Bipolar Mania

| Avoid Saying | Say Instead |

|---|---|

| “You ruined everything.” | “This caused real damage, and we need a plan to protect essentials.” |

| “You are irresponsible.” | “The spending pattern is not safe for our household.” |

| “I will never trust you again.” | “Trust will need to be rebuilt with clear safeguards.” |

| “You are not allowed to have money.” | “We need a plan that protects bills while preserving dignity.” |

| “This is all your fault.” | “Symptoms may be part of this, and responsibility still matters.” |

| “I will fix it like last time.” | “I cannot keep rescuing this without a long-term plan.” |

Words matter because shame can shut down repair. But avoiding the truth also prevents repair. The goal is honest, firm, non-humiliating language.

When Financial Boundaries May Become Financial Abuse

This article is about protecting a household from bipolar-related financial harm. It is not permission to control, isolate, intimidate, or punish a partner.

Financial abuse may include:

- controlling all money without discussion;

- withholding money for basic needs;

- blocking someone from working or studying;

- hiding assets;

- running up debt in someone else’s name;

- forcing someone to sign financial documents;

- threatening someone with homelessness or poverty;

- using a diagnosis to remove all independence;

- refusing access to medicine, food, transport, or safety resources.

If this sounds familiar, the problem may not be only bipolar disorder or overspending. It may involve abuse, coercion, or unsafe control. In the United States, you can contact The National Domestic Violence Hotline or use their warning signs guide. You may also find information through the National Network to End Domestic Violence.

Caregiver Guilt Is Not a Budgeting Tool

Many caregivers feel guilty when they set money boundaries. You may think:

- “If I loved them, I would help.”

- “They are sick, so I should not say no.”

- “What if my boundary triggers them?”

- “What if they think I am abandoning them?”

- “What if I am being controlling?”

Those questions are painful, but guilt is not a financial plan. Fear is not a debt strategy. Love is not a credit limit.

You can love someone and still protect rent. You can understand symptoms and still refuse to take on another loan. You can be compassionate and still say, “I cannot give money today.”

If you are constantly rescuing, hiding bills, lying to family, losing sleep, or living in fear of the next account statement, read how to support someone with bipolar without enabling. Support without boundaries can slowly become survival mode.

How to Rebuild Trust After Bipolar Manic Spending

Trust is not rebuilt by one apology. It is rebuilt by repeated, visible safety.

After a spending episode, rebuilding may include:

- naming what happened without minimizing it;

- reviewing the actual numbers;

- protecting the next month’s essential bills;

- agreeing on temporary spending limits;

- contacting the treatment team if symptoms were active;

- creating a debt plan;

- setting alerts or friction points;

- reviewing the plan during stability;

- getting caregiver support too.

A repair script may sound like this:

“I want to rebuild trust, but I cannot do that through promises alone. I need us to create a written plan for bills, debt, spending limits, and what happens if symptoms start affecting money again.”

When to Seek Professional Financial or Legal Help

Consider outside help if:

- debt is growing faster than you can track;

- you are missing essential bills;

- joint accounts are being drained;

- your credit is being damaged;

- you are being pressured to sign loans or documents;

- you are considering separation or divorce;

- there is bankruptcy, foreclosure, eviction, or tax debt;

- there is identity theft or coerced debt;

- you feel unsafe discussing money;

- you do not know your rights or obligations.

A nonprofit credit counselor can help you understand debt options. An attorney can help with legal rights, joint debt, divorce, housing, or protective steps. A domestic violence advocate can help if money is being used to threaten, trap, or control.

Do not wait until every account is empty before asking for help.

A Simple Financial Safeguards Checklist

- Protect rent or mortgage first.

- Protect food, medication, utilities, and transportation.

- List every debt and due date.

- Stop new non-essential purchases during active symptoms.

- Remove saved cards from shopping apps during stability if agreed.

- Turn on transaction alerts.

- Create a spending threshold.

- Create a 24 or 48-hour pause rule for non-essential purchases.

- Use a separate bills account if appropriate.

- Protect your own credit report if needed.

- Contact creditors before missed payments become worse.

- Consider nonprofit credit counseling.

- Talk to an attorney if legal risk is involved.

- Contact a domestic violence advocate if money is being used for control or threats.

- Add money safeguards to the bipolar emergency plan.

How This Fits With Other Caregiver Boundaries

Financial safeguards work best when they are part of a wider boundary plan. Money is only one piece of caregiving. You may also need limits around communication, crisis response, sleep, emotional labor, treatment refusal, and your own burnout.

These guides may help you build the full support system:

- Setting Boundaries With Someone With Bipolar Disorder

- What to Say When Setting Boundaries With Someone With Bipolar Disorder

- How to Communicate With Someone Who Has Bipolar Disorder

- Supporting a Spouse With Bipolar Disorder

- How to Support Someone With Bipolar Without Enabling

- What to Do When Someone With Bipolar Disorder Refuses Help

- Bipolar Caregiver Burnout

- How to Make a Bipolar Emergency Plan

Trusted Resources

- National Institute of Mental Health: Bipolar Disorder

- Bipolar UK: Bipolar and Money

- FTC: Credit Freezes and Fraud Alerts

- USAGov: How to Place or Lift a Credit Freeze

- National Foundation for Credit Counseling

- 988 Suicide & Crisis Lifeline

- The Hotline: Warning Signs of Abuse

- NNEDV: About Financial Abuse

Frequently Asked Questions

Can bipolar mania cause overspending?

Some people experience impulsive or risky financial behavior during mania or hypomania. This can include shopping sprees, gambling, risky investments, sudden generosity, subscriptions, travel, or major purchases. Not everyone with bipolar disorder overspends, but when it happens, it should be taken seriously.

What should I do first after manic spending?

Protect essentials first: housing, food, medication, utilities, transportation, and minimum debt payments. Then document the charges, contact banks or creditors if needed, and consider professional support. Avoid trying to solve the entire crisis in one emotional conversation.

How can I protect bills during bipolar overspending?

During stability, couples may use a separate bills account, automatic payments, spending alerts, purchase thresholds, and written agreements about what happens when symptoms affect money. The safest plans are clear, consent-based, and focused on essentials rather than punishment.

Should I hide money from my bipolar spouse?

A protected emergency fund can be reasonable, especially if housing, food, medication, or safety may be at risk. But secrecy can create new trust and safety problems. If you are hiding money because you fear retaliation, threats, or control, consider speaking with a domestic violence advocate or attorney.

Is it controlling to set financial boundaries with a bipolar partner?

Not automatically. It depends on how the boundary is created and used. A safeguard protects essential needs and dignity. Financial control uses money to punish, isolate, frighten, or remove independence. Collaboration during stability is safer than unilateral control during crisis.

Can I freeze my spouse’s credit during mania?

Generally, you should not try to freeze another adult’s credit without consent or legal authority. You can protect your own credit report, contact creditors about accounts in your name, and seek legal advice if joint debt, identity theft, or coerced debt is involved.

Does a credit freeze stop manic spending?

No. A credit freeze can make it harder to open new credit accounts in your name, but it does not stop spending on existing cards or accounts. It is one protection tool, not a complete financial safeguard plan.

What if my spouse refuses financial safeguards?

You cannot force another adult to agree to every safeguard. But you can decide what you will do to protect your own income, credit, housing, and safety. If refusal creates serious financial or safety risk, seek professional legal, credit, or domestic violence support.

How do we rebuild trust after bipolar manic spending?

Trust usually returns through repeated safety, not promises alone. Review the numbers, protect essentials, create a written plan, add spending friction, involve treatment or financial professionals when needed, and revisit the plan during stability.

When should I call 988 or emergency services?

If someone is suicidal, threatening harm, psychotic, violent, unsafe, or in immediate danger, call emergency services. In the United States, call or text 988 for crisis support. Financial damage matters, but safety comes first.

The Truth About What Saved Us

What saved us was not one perfect conversation.

It was not one apology. It was not one spreadsheet. It was not me becoming harder or them becoming instantly better.

What helped was structure.

We stopped pretending that love alone could protect the mortgage, the medication, the credit score, the grocery money, or the nervous system of the person trying to hold everything together.

We started writing things down. We separated emergency decisions from stable decisions. We protected essentials first. We stopped treating every financial boundary as a betrayal.

Financial safeguards did not remove the pain. But they gave us something to stand on when the next wave came.

If you are sitting at the kitchen table with bills open and your heart racing, start small. Protect the essentials. Write down the numbers. Ask for help. Build the plan during stability.

You can love someone with bipolar disorder deeply and still protect your financial safety. Those two truths can exist together.